Target date funds promise simplicity, but are you truly protected from market volatility as retirement approaches?

Understanding the Glide Path: How Target Date Funds Adjust Risk Over Time

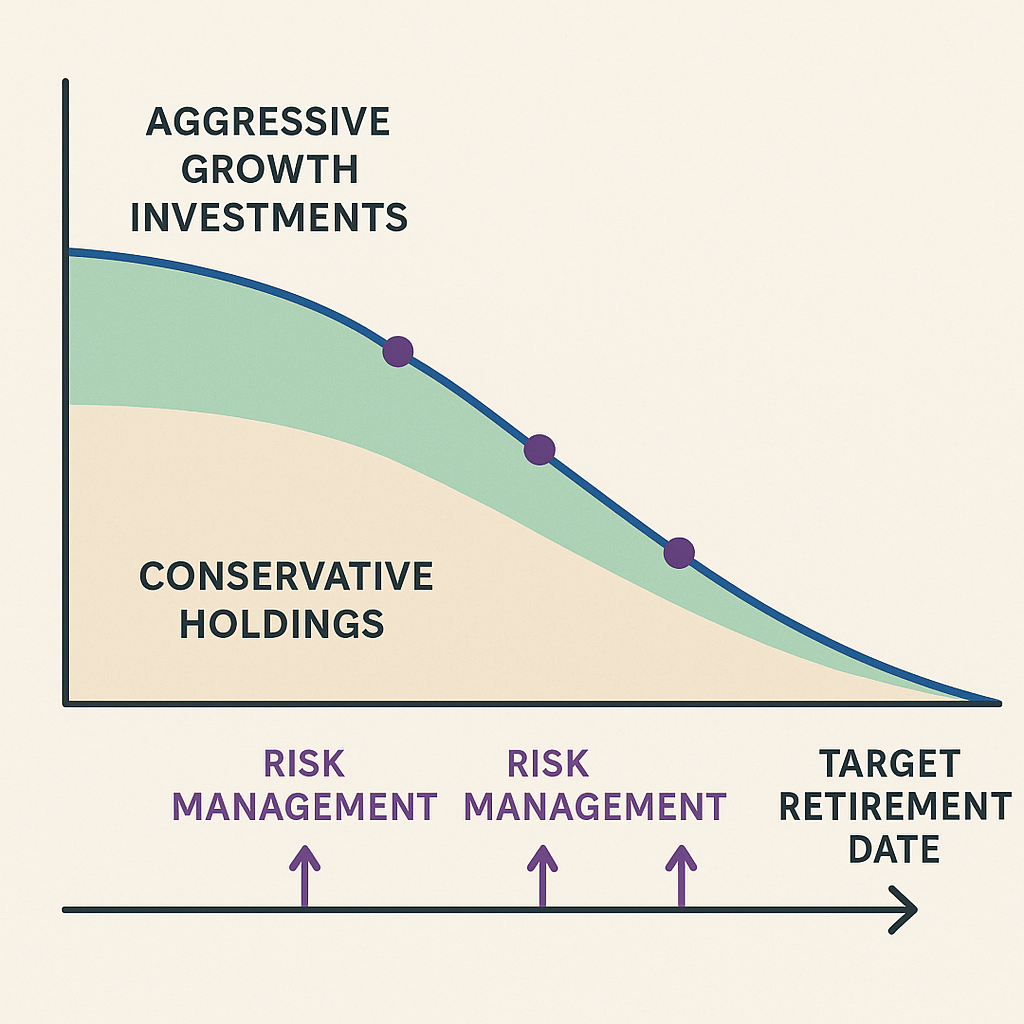

Target date funds have become the default investment option for millions of 401(k) participants, and for good reason. These funds operate on a fundamental principle called the glide path—a predetermined asset allocation strategy that systematically shifts from growth-oriented investments to more conservative holdings as your target retirement date approaches. But do you truly understand how this mechanism works and whether it aligns with your specific retirement income needs?

The glide path represents the fund manager's assumptions about risk tolerance over time. In your early career years, a target date fund typically maintains an aggressive allocation—often 90% or more in equities—capitalizing on your longer time horizon to weather market volatility. As you progress toward retirement, the fund gradually reduces equity exposure, increasing allocations to fixed income and stable value investments. This automatic rebalancing eliminates the need for active portfolio management, making target date funds particularly valuable for investors who lack the time, expertise, or inclination to manage their own asset allocation.

However, not all glide paths are created equal. Some funds follow a 'to retirement' approach, reaching their most conservative allocation at the target date itself. Others use a 'through retirement' strategy, continuing to adjust asset allocation for 10 to 20 years beyond the target date to account for longevity risk and the need for continued growth during retirement. The difference between these approaches can significantly impact your portfolio's ability to generate income throughout a retirement that may span three decades or more. Understanding which philosophy your target date fund employs is essential for determining whether it appropriately manages risk for your individual circumstances.

Beyond the Target Date: What Happens When Retirement Actually Arrives

The target date printed on your fund's name—2030, 2040, 2055—creates a psychological anchor that may not reflect the complexity of actual retirement. What happens when that date arrives? Many investors assume the fund becomes entirely conservative, preserving capital for immediate withdrawal. The reality is far more nuanced and requires careful consideration as part of your comprehensive retirement income strategy.

Most target date funds don't stop adjusting at the target date. Funds following a 'through retirement' glide path continue to hold significant equity exposure—often 30% to 50%—well into your retirement years. This approach acknowledges a critical financial planning reality: retirement isn't a single moment but rather a potentially decades-long phase requiring ongoing growth to combat inflation and support longevity. For a 65-year-old in good health, retirement planning must account for the possibility of 25 to 30 years of living expenses, healthcare costs, and lifestyle goals.

This extended equity exposure introduces a question every pre-retiree should consider: does your target date fund's post-retirement allocation align with your withdrawal strategy and risk capacity? If you plan to transition substantial assets into guaranteed income vehicles or maintain conservative spending rates, your target date fund's continued equity exposure might represent more volatility than necessary. Conversely, if you're planning for longevity with flexible withdrawal strategies, the fund's growth component may prove essential. The target date is a milestone, not a finish line—and your retirement income planning should reflect this reality.

Additionally, consider how the target date fund fits within your broader financial picture. High-net-worth individuals and business owners often have multiple income sources—Social Security, pensions, business succession proceeds, real estate income, or taxable investment accounts. Your 401(k)'s target date fund represents just one component of a comprehensive wealth management strategy. Evaluating whether the fund's risk profile complements or duplicates risk elsewhere in your portfolio requires the kind of holistic analysis that connects personal wealth management with retirement plan assets.

Evaluating Asset Allocation and Diversification Within Your Target Date Fund

Target date funds offer diversification by design, but are you examining what's actually inside these seemingly simple investment vehicles? Most target date funds are 'funds of funds'—they hold shares of multiple underlying mutual funds or collective investment trusts, each focused on different asset classes. This structure provides broad diversification across domestic equities, international stocks, investment-grade bonds, and sometimes alternative investments. However, the quality and appropriateness of this diversification varies significantly across fund families.

When evaluating your target date fund's asset allocation, look beyond the simple equity-to-fixed-income ratio. Examine the geographical diversification: what percentage is allocated to international developed markets versus emerging markets? Consider the equity style exposure: is the fund balanced between growth and value stocks, or does it tilt toward one investment style? Review the fixed income composition: are you holding primarily government securities, corporate bonds, or a mixture that includes high-yield debt? These underlying allocation decisions materially impact both risk exposure and expected returns.

The diversification question becomes particularly important when considering concentration risk. Some target date funds use underlying funds exclusively from their own fund family, which may limit access to specialized asset classes or specialized investment managers. Other funds take a more open architecture approach, selecting from a broader universe of investment options. Neither approach is inherently superior, but understanding the construction philosophy helps you assess whether the fund provides genuine diversification or simply packages multiple correlated investments together.

Furthermore, consider whether your target date fund incorporates strategies aligned with your values or risk management priorities. Does the fund include environmental, social, and governance (ESG) screening? Are there inflation-protected securities to hedge against purchasing power erosion? Does the international allocation hedge currency risk? These questions move beyond basic diversification into the realm of sophisticated risk management—the kind of analysis that professional advisors employ when constructing institutional-grade portfolios. Your 401(k) may be a workplace benefit, but it likely represents a substantial portion of your retirement assets and deserves this level of scrutiny.

Hidden Risks That Target Date Funds May Not Address

Target date funds excel at managing market risk through systematic asset allocation adjustments, but several important risks fall outside their design parameters. Recognizing these blind spots is essential for determining whether a target date fund alone provides adequate retirement security or whether supplemental strategies are necessary.

Sequence of returns risk represents perhaps the most significant vulnerability for target date fund investors nearing retirement. This risk arises when negative market returns occur during the years immediately before or after retirement—precisely when your account balance is largest and you're beginning withdrawals. Two investors with identical contribution histories and average returns can experience vastly different retirement outcomes based solely on the timing of market volatility. While target date funds reduce equity exposure as retirement approaches, they typically maintain sufficient market exposure that a significant downturn can substantially impact your retirement readiness. The 2008 financial crisis provided a stark illustration of this risk for investors with 2010 target date funds.

Longevity risk—the possibility that you'll outlive your assets—receives only partial consideration in target date fund design. While 'through retirement' glide paths acknowledge extended retirement timelines by maintaining growth-oriented investments, the fund itself has no mechanism for managing withdrawal rates or adjusting to your actual spending needs. A target date fund doesn't know whether you plan to withdraw 3% or 7% annually, whether you have pension income, or whether your healthcare costs will be higher than average. These individual factors dramatically affect whether your portfolio will sustain you through retirement.

Inflation risk also merits careful consideration. Fixed income investments protect against volatility but historically underperform relative to inflation over extended periods. As your target date fund shifts toward bonds, your portfolio becomes more vulnerable to purchasing power erosion—particularly concerning given that healthcare costs, a major retirement expense, typically inflate faster than general consumer prices. Some target date funds incorporate Treasury Inflation-Protected Securities (TIPS) or other inflation-hedging strategies, but many do not, leaving this risk largely unmanaged.

Finally, target date funds cannot address tax diversification or tax-efficient withdrawal strategies. Your 401(k) assets are tax-deferred, meaning every distribution will be taxed as ordinary income. This tax treatment differs from Roth accounts, taxable brokerage accounts, or municipal bonds, each offering distinct tax characteristics. Comprehensive retirement income planning requires coordinating withdrawals across multiple account types to manage tax liability—a form of risk management that exists entirely outside your target date fund's capabilities. Business owners and high-income professionals, in particular, benefit from sophisticated tax planning that coordinates retirement account withdrawals with business succession strategies, estate planning techniques, and other wealth management considerations.

Fiduciary Considerations for Plan Sponsors Selecting Target Date Funds

For HR managers, benefits administrators, and CFOs responsible for 401(k) plan oversight, selecting and monitoring target date funds carries significant fiduciary implications under ERISA. The Department of Labor has provided guidance emphasizing that plan sponsors must conduct a prudent process when selecting target date funds as qualified default investment alternatives (QDIAs)—and that responsibility doesn't end once the fund is selected.

The fiduciary selection process requires evaluating target date funds across multiple dimensions. Fee structures demand particular attention: expense ratios for target date fund suites can range from under 0.15% for low-cost index-based options to over 1.00% for actively managed alternatives. Over a 30-year career, this difference compounds dramatically—a $50,000 investment growing at 7% annually with 0.15% fees results in approximately $360,000, while the same investment with 1.00% fees produces only $270,000. Plan sponsors must document why selected fee levels are reasonable relative to services provided and participant outcomes.

Glide path evaluation represents another critical fiduciary responsibility. Plan sponsors should understand whether their selected target date fund family employs a 'to' or 'through' retirement approach and why that philosophy aligns with their participant population's needs. What is the fund's most aggressive allocation for participants far from retirement? What equity exposure remains at the target date and beyond? How does the transition occur—gradually over decades or more precipitously as retirement approaches? These design choices reflect fundamental assumptions about participant behavior, risk tolerance, and retirement income needs that plan sponsors must evaluate and periodically reassess.

Monitoring requirements extend throughout the fund's tenure in your plan. Has the fund family changed its glide path methodology? Have key portfolio managers departed? How has performance compared to peers with similar risk profiles—not just in bull markets but during periods of volatility? Are participants receiving adequate education about how target date funds work and their role within comprehensive retirement planning? ERISA's prudent expert rule holds plan sponsors to a high standard of ongoing diligence, and the Department of Labor has indicated that simply selecting a target date fund and walking away does not satisfy fiduciary obligations.

Plan sponsors should also consider whether target date funds should be supplemented with additional investment education and resources. While these funds provide a reasonable default for participants who don't actively select investments, they're not optimal for everyone. High earners may benefit from more aggressive allocations than standard glide paths provide. Participants with defined benefit pensions can typically tolerate more equity risk in their 401(k) accounts. Those planning early retirement need asset allocation strategies aligned with earlier withdrawal timelines. Providing participants with access to financial education, planning tools, or professional advisory services—potentially including coordination with personal wealth management strategies—enhances the value proposition beyond simply offering target date funds as a default option.

Organizations committed to attracting and retaining top talent recognize that retirement benefits represent a competitive differentiator. A thoughtfully selected and monitored target date fund suite, embedded within a comprehensive retirement plan supported by education and fiduciary governance, signals to employees that their long-term financial security matters to their employer. This commitment becomes particularly important when competing for executives, professionals, and key personnel who evaluate total compensation—including retirement plan quality—when making career decisions. Fiduciary excellence in plan oversight isn't merely a compliance obligation; it's a strategic advantage in the talent marketplace.